The Fallacy of Strategic Uncertainty

There is no order to chaos in Trump 2.0, especially when it comes to the tariff war.

The MAGA crowd likes to call it “strategic uncertainty” — implying that there is a grand plan to the chaos of Trump 2.0. Economists are more agnostic, holding the view that uncertainty is the enemy of decision making, especially key elements of business decision making like capital spending and hiring. This is a critical distinction that is likely to have important implications for the economic and financial market outlook.

Scott Bessent, like many Yale undergrads, probably took an introductory course in game theory. As US Treasury Secretary, he appears to be dusting off his old class notes. At least that’s the inference that can be drawn from his reference to Thomas Schelling’s work on conflict and cooperation. It is also apparent in Bessent’s emphasis on the key role that strategic uncertainty can play as a negotiating tool for the purported brilliance of a deal-focused President Trump. By “flooding the zone” — more than 150 executive orders in the first 115 days of Trump 2.0, along with at least 50 modifications in US tariff policy — Magaspeak maintains that America’s opponents will succumb to the broken spirit of fear and confusion and surrender under pressure. Try telling that to the Chinese, where State media has been quick to celebrate last weekend’s Geneva Accord as a brilliant negotiating triumph for the nation’s “defiant response” to Trump’s tariff attack.

Putting aside self-serving claims from both sides, there can be no mistaking the dramatic shift in the US position. Apart from China, all the so-called reciprocal tariffs of Liberation Day were quickly put on pause as financial markets imploded. Now, by rolling back 80% of the absurdly excessive 145% tariffs that an angered US President imposed on China in a retaliatory tantrum, the last of the reciprocal tariffs has been suspended. In contrast to the dramatic action that on April 2 Donald Trump characterized as a “ … declaration of economic independence … the day that America’s destiny was reclaimed,” it now looks like Liberation Day has, indeed, morphed into Capitulation Day.

Secretary Bessent can dub this back-and-forth anything he wants, but the key point for economies and markets is that the policy volatility and uncertainty of the past 115 days is not an aberration. Donald Trump, who dashed off on a deal-focused junket to the Middle East the very same day the details of Geneva Accord were revealed, thrives on chaos. Don’t expect this so-called pause on reciprocal tariffs to lead to a cooling off of trade tensions. De-escalation, as Bessent hinted prior to the meetings in Geneva, was a no-brainer relative to existing tariff rates of 145%. But that doesn't rule out the high likelihood of additional actions and counteractions during and after the current pause.

The significance of that conclusion should not be lost on business decision makers, policymakers, and financial markets. Ultimately, the verdict is less about anecdotes and political bluster, and more about an empirical assessment of policy uncertainty. The chart below illustrates a well-known metric of “trade policy uncertainty” based on a carefully designed statistical index of the frequency of references to trade policy in ten major US newspapers. It can be found on the Economic Policy Uncertainty website and is based on a peer-reviewed article in a highly respected academic journal.

The chart speaks for itself. Never before has US trade policy uncertainty (TPU) come close to approaching the readings that are currently evident. The latest reading for April 2025 hit a level over four times that reached during the initial Trump tariffs of 2018-19. Of course, back then, those were largely China-centric actions, considerably narrower, and far less extreme, than the broad and more onerous multilateral actions of 2025. Not shown, but also available on the EPU website, is a daily metric of trade policy uncertainty; the latest data point for May 13 (yesterday) was 33% above the April 2025 average. So much for the purported windfall of de-escalation!

My basic point is that the memory of this experience will not fade quickly, if at all. Even if the post-Liberation Day pause turns out to last, President Trump, true to his reputation as “Tariff Man,” believes in the permanent floor of 10% tariffs for all of America’s trading partners. He sees it as the price they must pay for “ripping us off” over most of the last 75 years. As I pointed out in my previous post, this 10% “universal tariff” represents more than a five-fold increase from the 1.8% average effective US tariff rate over the past thirty years (1995 to 2024). This quantum shift in America’s tariff regime, in conjunction with a major push toward “friendshoring” and a related realignment of global supply chains, underscores the likely persistence of elevated readings of trade policy uncertainty for many years to come.

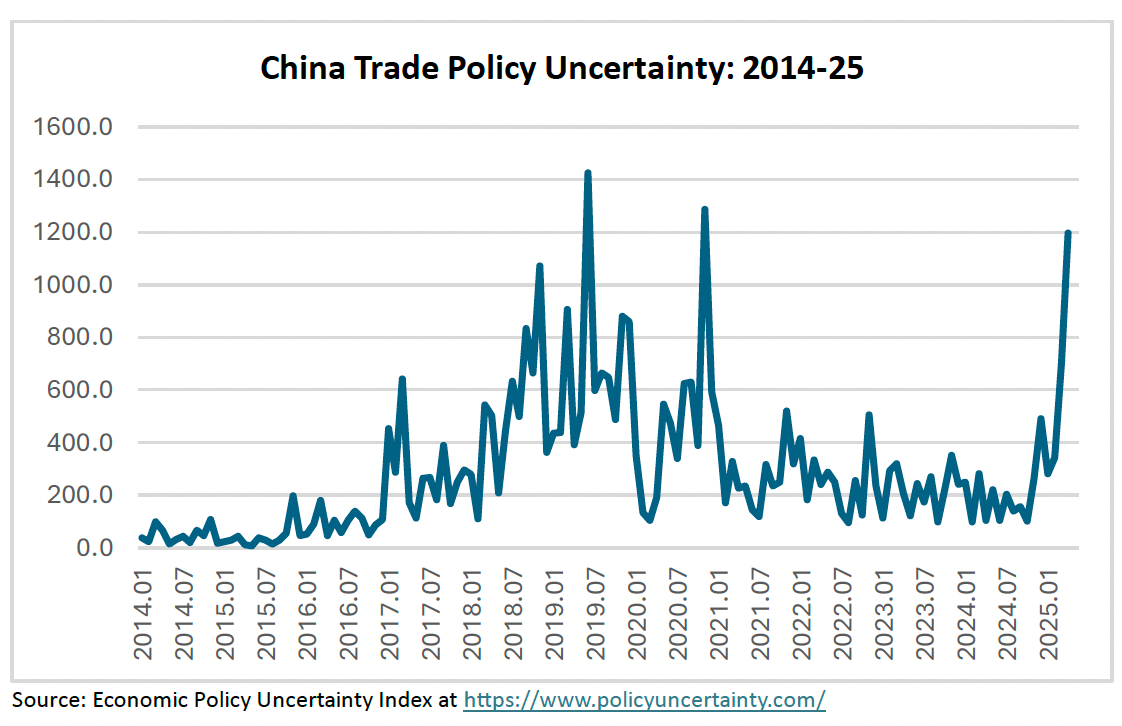

The United States, while the instigator of this tariff war, is hardly alone in feeling the seismic impacts of trade policy uncertainty. The chart below provides a similar metric for China. Like the United States, there has been a dramatic spike in early 2025. But unlike the US, China’s current uncertainty shock is quite comparable to that which it experienced in 2018-19, when it was hit by the initial tariff hikes of Trump 1.0.

China learned a good deal from this earlier experience. The legacy effects of Trump 1.0 have had an enduring impact on the Chinese policy mindset. As a result, China was better prepared for what was to come in Trump 2.0. While it certainly did not expect the extreme actions that were taken in April — actions that were initially dubbed to be a “a joke” by Chinese officials — China’s export diversification strategy of 2020-23 focused on shifting the mix of its exports away from the US to other markets, especially Vietnam, Russia, and India. While that has proved to be successful in tempering the initial blow of a sharp contraction of Chinese exports to the US — off 21% y/y in April while overall exports still rose 8% — export-dependent China remains vulnerable to a likely broader downturn in the global trade cycle.

All this gets back to the point I mentioned at the outset: Persistent levels of trade policy uncertainty are not a strategic benefit of a chaotic policy of adversarial confrontation; instead, protracted uncertainty is more likely to take a serious toll on business decision making, especially for multinational corporations who operate and source from around the world. It will be exceedingly difficult for global companies to plan in this new era of uncertainty. That will draw considerations of future scale into sharp question, crimping capital spending and hiring plans as a result, with major knock-on effects for personal income generation and aggregate consumer demands.

As evidenced by the sharp rebound from the post-Liberation Day swoon, financial markets are always quick to forget yesterday’s shock and eager to move on to the next development, the next theme — de-escalation in this case. Corporate decision makers have deeper memories — underscoring the distinct possibility of a lasting toll from elevated levels of trade policy uncertainty. I still believe that’s likely to be the case in the US, China, and the rest of the world economy.

There is a unified theory of Trump and it’s simple as it only has three pillars:

1) Policy Goal: Extend the expiring tax cuts via reconciliation. This was his only achievement in Trump 1.0 and to do this he must demonstrate the tax cuts will be revenue neutral so raising import taxes and cutting government services and all forms of foreign aid are part of this.

2) Personal Enrichment: Make as much money for himself and family as possible. This is so insidious and audacious as per everything from NFTs and gold sneakers to cryptocurrency bribes and 747 airplanes. This is the greatest corruption in American history.

3) Personal Protection: He is still a convicted felon so he must destroy and control any institutions which may challenge him such as law firms, judges, universities, think tanks, prominent individuals, the media, democrats, moderate “Republicans”, foreign leaders, etc etc.

4) Maintain the Base: Flood the media with propaganda, lies and distortions to confuse and distract the media and ultimately the public to keep pressure on Congress and threaten any individual or institution that may challenge him. Immigrants playing a desperate role here.

Everything Trump (or Krasnov as the KGB / FSB calls him) does falls into one of these pillars of tyranny and fascism.

As stated in King Lear; ‘Tis the time’s plague, the madman leads the blind.

To your broader point, two of the principal targets of the TPU “strategy” (Canada and China) are diversifying away from US markets and into stronger bilateral ties.