The Doublespeak of China's Anti-Involution Campaign

Another high-profile attempt to micromanage the supply side while ignoring the demand side

No matter what the Chinese leadership calls it — supply-side structural reform, the excess capacity overhang, dual circulation, or now, anti-involution — the message remains the same: the broad thrust of all these initiatives aims to bring aggregate supply into better alignment with aggregate demand.

In one sense, this focus is surprising, With its legacy of central planning, one might think that Chinese policymakers would be especially adept at getting the supply side right. But this sequence of supply-side initiatives says otherwise. And it deflects attention away from the very real problems remaining on the demand side.

The stakes are especially high today. China now faces the ultimate test of seemingly chronic supply-demand imbalances — the risks of a protracted deflation. As measured by the overall GDP deflator, the aggregate Chinese price level is estimated to have declined by an average of 0.5% per year over the 2023-25 interval (factoring in a 0.3% decline in 2025 as per the IMF’s latest forecast). By comparison, this is a steeper pace of deflation than that experienced by Japan in the early stages of its first “lost decade” — a 0.1% average decline in the Japanese GDP deflator from 1995 to 1998 that was then followed by a far more serious deflation averaging 1.1% per year over the next decade, from 1999 to 2008.

The lessons of Japan remain an important consideration in the Chinese policy debate. Since 2016, dating back to the famous “authoritative person” interview published on the front page of People’s Daily, the risks of a Japan-style deflationary stagnation have been widely discussed in Chinese policy circles. These concerns were once again heightened by the release of China’s latest price statistics, a surprisingly steep -0.4% decline just reported in the August CPI.

The early signs of a persistent deflation have spawned concerns over involution (in Chinese, “neijuan” (内卷)) — a concept borrowed from sociology that has been embraced by senior Party officials, including Premier Li Qiang, to refer to price declines arising from disorderly, overly-aggressive competition in several key industries. Anti-involution policies like corporate restructuring (i.e., downsizing and increased M&A activity) and increased regulatory oversight have so far focused on several of China’s new advanced industries, including EV batteries, solar power equipment, and autos but also in more traditional sectors such as steel, cement, coal, chemicals, and glass, as well as airlines and express delivery services.

The notion of “overly aggressive” competition is a relative construct. It makes best sense when judged against conditions on the demand side. That’s what links involution to the earlier debate over excess Chinese capacity that many wrote about last year. Ironically, Xi Jinping’s recent emphasis on growth in “new productive forces” may well be an important part of China’s involution problem in that it has led to a rapid expansion of new entrants into many of the nation’s most advanced industries. That has become especially problematic as China’s excess supply has become increasingly disruptive to foreign markets, contributing to a mounting protectionist backlash. The key to a successful anti-involution campaign may well lie in redirecting Chinese supply away from overly saturated external markets toward untapped domestic demand.

That, of course, won't be easy. China’s deficiency of domestic demand — especially household sector consumption — is well known and a topic that I have been addressing in my own research and commentary for at least fifteen years. It is especially relevant to the Japan comparison, noted above. A key and very worrisome difference between China and Japan is that China has a far more serious problem than Japan with its imbalance between excess supply and deficient consumer demand.

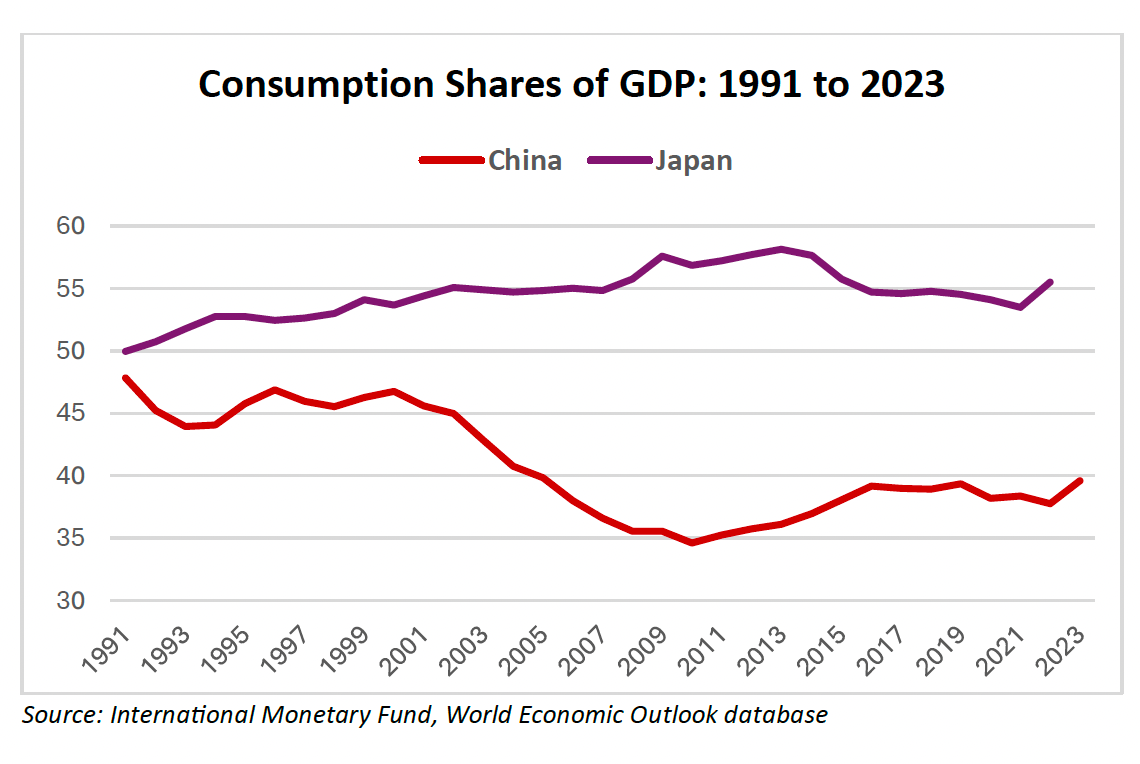

This is evident in the chart below, which compares private consumption shares of GDP for Japan and China from 1991 to 2023. During Japan’s first lost decade, a period roughly spanning from 1992 to 2001, its household consumption share averaged 52.8%. This is fully 14 percentage points above the 38.6% average household consumption share in China over the most recent three years, 2021-23 (latest data available).

China’s seemingly chronic problem of subpar household consumption has long stood in sharp contrast with Japan’s much higher consumption share, which is in broad conformity with shares in most other developed nations — apart, of course, from the excess consumption extremes of the US. That means, at least from the standpoint of supply-demand imbalances, Japan was in much better position to address its emerging deflation problem in the 1990s than China is in today.

Notwithstanding its higher consumption share, Japan has still struggled mightily to extricate itself from a subsequent string of two additional lost decades. While this is the subject of countless books, research papers, and commentary, my own preference is to examine the Chinese version of the Japanese lost-decade conundrum through the “three arrow” lens of the late Prime Minister, Shinzo Abe. As seen from this perspective, Japanese policymakers were too slow to respond with the first two arrows of monetary and fiscal stimulus, respectively, but ultimately were stymied by political constraints on the third arrow, structural reforms. As I wrote last year in the Financial Times, it remains to be seen if Beijing has learned this important lesson.

China’s anti-involution campaign seems to be addressed more to the symptoms than to the source of the problem. Drawing on the micromanagement of its central planners — especially the National Development and Reform Commission — to deal with industry-specific price setting, runs the risk of mistaking the trees for the forest. Unlike Japan, China suffers from a serious deficiency of household consumption that, in my view, can only be addressed by reducing the excesses of fear-driven precautionary saving through dramatic improvements in a still inadequate social safety net.

Without greater support from consumer demand, the Chinese economy remains at risk of falling into a Japanese like quagmire. Like Japan during the late 1980s and early 1990s, China’s mounting debt-intensity, in conjunction with the bursting of major asset bubbles (property, and, to a lesser extent, equities), suggests that the possibility of a prolonged balance sheet recession remains a legitimate concern. Moreover, the old version of the Japanese financial system, hobbled by the interplay between underwater bank loans and an insidious implosion of zombie corporate keiretsus, is not all that dissimilar from the Chinese counterpart of interlocking state-owned enterprises and government-directed policy banks.

Sure, the Chinese economy is still growing at roughly a 5% annual rate, fully seven times the nearly stagnant pace of Japan’s 0.7% average growth from 1992 to 2024. But for a nation which had become accustomed to 10% growth from 1980 to 2010, the deceleration in underlying Chinese GDP growth of 5 percentage points from its high-growth norm is a big deal; moreover, this downshift is expected to widen further to 6.5 percentage points by 2029-30 (according to the latest medium-term baseline forecast of the IMF). On a relative basis, China’s growth slowdown is very similar to Japan’s deceleration from 7.25% average growth from 1946-90 to just 0.7% post-1991. In other words, compared with the hyper-growth trajectory of the past, the current and coming deceleration in the Chinese economy would qualify as a legitimate Japanese-style growth shock.

The new anti-involution campaign will do little to buffer the impacts of China’s growth shock. Like earlier actions aimed at tinkering with the supply side, it suffers from the legacy effects of one of central planning’s greatest shortcomings — ignoring the demand side. China’s anti-involution campaign risks micromanaging an increasingly daunting macro problem.

A few years ago I remember reading that Xi said something to the effect that consumerism is bourgeois. That’s obviously not the right attitude for a leader who needs to increase consumer spending.

Professor Roach’s comment on a lack of a good social safety net encouraging savings at the expense of spending makes perfect sense.

I was told that the per capita dollar amount needed to meaningfully increase consumer spending is actually quite small, perhaps several hundred dollars. I don’t know if that is correct.

Separately, I think that the inability of the government to have real estate taxes in most of the country is a problem: if municipalities don’t have that source of income they will be pressured to keep selling land, which creates excess real estate inventory, with the attendant negative consequences. My opinion, anyway.

Stephen, I wonder whether there is a limit to the relevance of the Japanese comparison. Japan was already a developed country when the bubble burst; Chinese GDP per capita remains less than half that of Japan even today. Isn’t this relevant to the demand side comparison? A substantial portion of the Chinese population continues to live at very low levels of income; how realistic it to expect consumption to assume as great a role as suggested while thus remains so? Reducing residential real estate as a share of the economy has been an objective, although progress has been slow and not necessarily arising from only from government policy. Regarding the social safety net, while the government has said there remains room for further development, Xi has also warned against “welfarism” leading to laziness and high cost. Plenty of cautionary examples in Western countries on this front.

It used to be common to wonder if China would rich before it got old. It’s hard to imagine that it could have run any faster than it did over the past years to try to win that race, but as yet the danger persists that it will not. Excesses and gaps arose accordingly during that sprint. It made hay while the sun shone (WTO membership was the sun) but clouds have returned before all the crop was in. Now what - just add 1-2 generations to the time scale perhaps?