Why China Needs a "Three Arrows" Strategy

Financial Times opinion: October 1, 2024

Beijing should err on the side of acceptance rather than denial and make major efforts to avoid the mistakes of Japan.

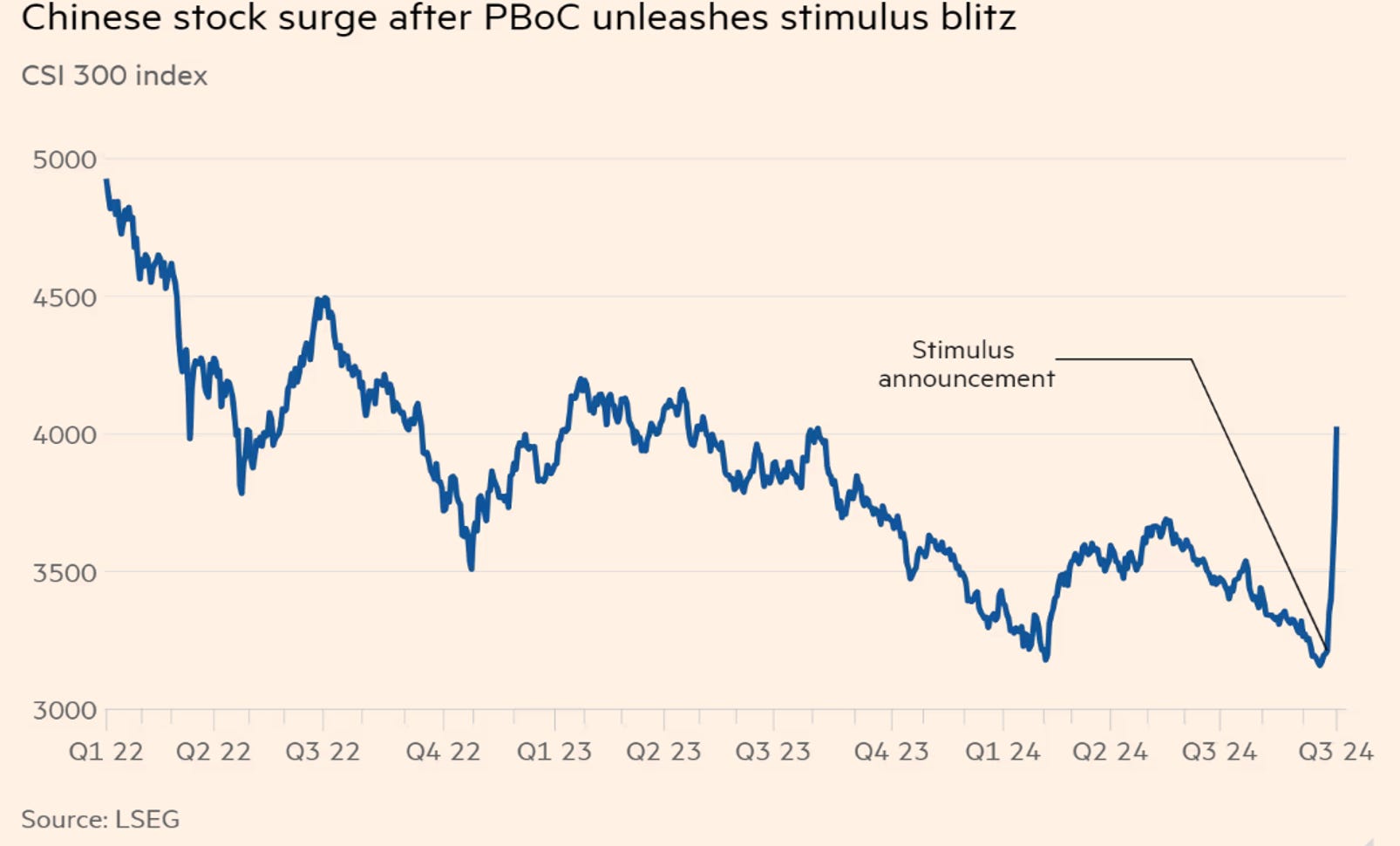

China’s seemingly outsize policy stimulus last week took many of us by surprise. The nation’s financial authorities apparently came to the rescue with their own version of a “big bazooka”. At least that was the initial verdict of an explosive rally in the Chinese equity market. With the Chinese Communist party’s Politburo sending a message of more to come, is the country’s long economic nightmare now over?

If it were only that easy. China is at risk of falling into a Japanese-like quagmire characterized by stagnation and deflation as a result of the bursting of a major debt-fueled asset bubble. The comparison is far from perfect. China still has untapped sources of future growth — namely, household consumption, urbanization and insufficient capital endowment of its large workforce. China also benefits from understanding the lessons of Japan as underscored by a famous warning on the issue by an unnamed but “authoritative person” on the front page of People’s Daily back in May 2016.

Being forewarned, however, is not the same as being pre-emptive. The jury is still out on whether China has succumbed to the Japanese disease. But Chinese policymakers should err on the side of acceptance rather than denial of the need for action.

China has experienced its most severe whiff of deflation since the 1980s, as well as a growth shock on a par with that in Japan. China’s GDP growth rate is decelerating by six percentage points from the 10 per cent surge from 1980 to 2010 to the IMF’s projected increase of around 4 per cent over the next five years, virtually the same as that which hit Japan when its economic growth went from 7.25 per cent from 1946-90 to just 0.8 per cent from 1991 to 2023.

Japan not only provided a template of what to avoid but the “Abenomics” framework of the late prime minister Shinzo Abe offered a prescription for how to get out of the quagmire. It was broken down into three “arrows”, as Abe dubbed them — monetary, fiscal, and structural. The theory was simple: powerful fiscal and monetary stimuli were necessary to provide Japan with escape velocity while structural reforms were vital for an enduring recovery. In the end, Japan lacked the political will for the heavy lifting of structural change. Could the same fate await China?

Beijing’s latest financial stimulus appears to be an impressive first arrow. Large interest rate cuts — coupled with major liquidity injections into hard-pressed local governments and a beleaguered equity market — are especially significant. However, despite the seemingly extraordinary 25 per cent in the surge CSI 300 Index following China’s policy pronouncements, the market remains fully 31 per cent below its February 2021 high. The Japanese experience provides an important perspective, as the Nikkei 225 Index bounced four times by an average of 34 per cent on its way to a 66 per cent cumulative drop from December 1989 to September 1998.

China’s fiscal arrow is iffier. In the Politburo statement, actions were framed more by broad promises than specifics. For example, a pledge to support the property market was couched mainly in terms of cuts in mortgage rates and downpayment requirements for second homes. There was no detail on absorbing the overhang of unsold homes. Like Japan in the 1990s, Beijing remains wary of deploying a fiscal bazooka as it did in 2009-10, given mounting public-sector indebtedness. That’s understandable, with the Chinese government’s debt-to-GDP ratio at 85 per cent in early 2024, nearly three times what it was back then (33 per cent in 2009-10).

As it was for Japan, structural reform is the most problematic arrow for China. It faces three major structural challenges: demographic, productivity and chronic under consumption. The Communist party’s recent Third Plenum took steps to address some issues, but this was mainly a disappointingly small and glacial rise in China’s absurdly low retirement age.

Meanwhile, actions in support of the once-dynamic private sector are more rhetorical than substantiative in rolling back regulatory and political constraints that have been in place since mid-2001. Nor has Beijing faced up to China’s most daunting third-arrow impediment to structural rebalancing — social safety reforms (ie retirement and healthcare) needed to reduce excessive fear-driven saving and boost discretionary household consumption.

With the markets roaring their early approval of China’s bold policy actions, it is tempting to say that the worst is over for the country’s beleaguered economy. At best, that conclusion is premature. At worst, it is a false dawn. At a minimum, the three-arrow framework warns against cracking out the champagne in response to Beijing’s latest pronouncements.

They should have let in American private equity and MBAs to come in to asset strip and un-clog the corporates in Japan. The government and banks still prop up a lot of unprofitable legacy businesses.

This piece echoes the doubts expressed by George Magnus on CNBC yesterday.