Trump 2.0 and China

The re-run of an old movie on steroids

Donald Trump’s possible ascension as the “MAGA unity” candidate promises a series of seismic shocks to the US political landscape. This is likely to be especially evident with respect to his policies toward China. In many respects, this is a rerun of an old movie. As I wrote in the Financial Times in the early months of his presidency, Donald Trump has never understood tariffs and trade deficits and how they fit into the macro structure of large economies. All these years later, he remains afflicted by the same “trade-deficit disorder” that shaped his anti-China policies from 2017 to 2020.

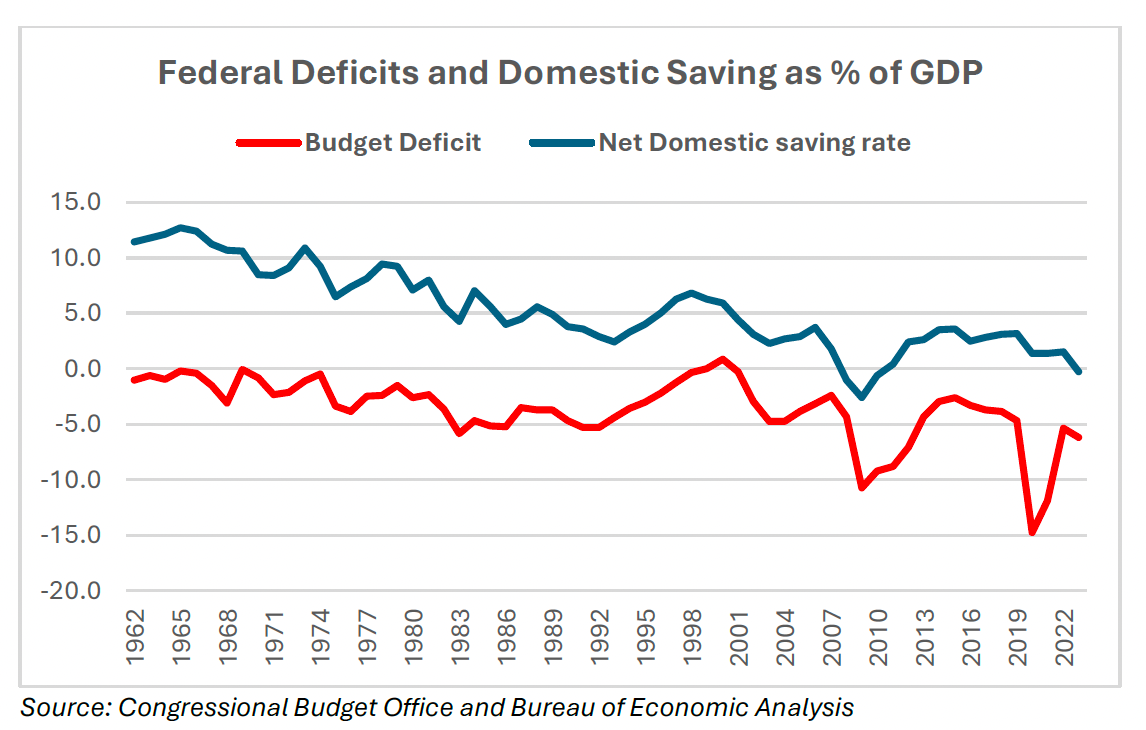

This disorder stems from the implications of America’s profound shortfall of domestic saving — exemplified by a net national saving rate that was -0.3% of national income in 2023. Lacking in saving and wanting to invest and grow, the United States must import surplus saving from abroad; the resulting balance-of-payments deficit, which hit 3% of GDP in 2023, leads to a large multilateral trade deficit with many countries. In 2023, the US ran merchandise trade deficits with 106 nations.

There is no dark secret as to the major source of America’s domestic saving problem — the dissaving that comes from massive, chronic federal budget deficits. That suggests that federal deficit reduction would be the single most effective policy strategy to cut the multilateral trade imbalance, to say nothing of reducing the major bilateral pieces of that gap with countries like China. Yet that seems highly unlikely in the years ahead. The latest CBO baseline projection calls for average federal budget deficits of -5.6% of GDP in the decade ending 2033 — well in excess of the -3.2% average from 1962 to pre-Covid 2019.

While that baseline projection is largely based on a Biden” current-policy” trajectory, there is little reason to expect much relief in a Trump 2.0 administration, especially with Trump’s promises to restore earlier large tax cuts. By way of perspective, federal budgets over the combined seven years of Trump 1.0 and the Biden era (2017 to 2023) have averaged -7.2% of GDP, more than double the long-term pre-Covid average. With Trump and Biden collectively having been America’s most deficit-prone presidents, trade-deficit disorder is very much a bipartisan pathology. Neither political party is willing or able to look in the mirror to resolve budget or trade imbalances.

Instead, rather than face up to US deficit reduction and domestic saving imperatives, Washington politicians have long opted for the trade deficit blame game, in effect, harboring the false believe that the US can eliminate its trade deficit by leaning on the imbalance with its largest trading partner. This “bilateral bluster,” as I dubbed it in Chapter 4 of my last book, Accidental Conflict, has repeatedly backfired. We tried that approach with Japan in the 1980s and it failed. Trump tried the same strategy with China with sharp tariff increases in 2018-19, and that approach also failed. While the US-China imbalance narrowed, there was no relief for saving-short America — the overall merchandise trade deficit widened by $181 billion from 2018 to 2023.

Alas, there was an important twist: With the Chinese piece of the US trade deficit shrinking but the overall trade deficit getting worse, there can be no mistaking the powerful repercussions of trade diversion. In the face of a persistent shortfall of domestic saving, the portion of America’s multilateral trade deficit that had been going to China was, in fact, diverted to other foreign producers — namely, Mexico, Vietnam, Canada, South Korea, Taiwan, India, Ireland, and Germany.

This leads to what may well be the most insidious symptom of trade-deficit disorder — that it imposes the functional equivalent of a tax hike on American families. In large part, that’s because trade diversion pushes the mix of the US merchandise trade imbalance disproportionately toward higher-cost foreign producers. I noted recently that about 70% of the trade diversion away from China since 2018 went to higher- or comparable-cost nations, whereas only about 25% went to lower-cost US trading partners like Vietnam and India. Look for more of the same in a Trump 2.0 administration, with further misdirected efforts to achieve the impossible — a bilateral fix for a multilateral saving problem.

But it’s not just trade diversion that is likely to be so problematic as Trump ups the ante on the China solution to America’s trade deficit. Candidate Trump has proposed that US tariffs on Chinese imports, which have gone from 3% in early 2018 to 19% currently (covering 66% of Chinese goods exports to the US), should rise to 60% on all imported Chinese products. Contrary to what Trump the “tariff man” thinks — that tariffs are a tax on Chinese exporters — tariffs raise the costs of US imports. Recent Peterson Institute research finds that Trump 2.0 anti-China tariffs would generate added costs of at least 1.8% of GDP, nearly five times that of Trump’s first round of tariffs; that works out to about a $1,700 tax on the average US household, with regressive impacts especially acute at the lower end of the income distribution.

This underscores the double-whammy of Trump’s efforts to intensify pressures on China — the direct cost increases associated with sharply higher tariffs on Chinese imports and further trade diversion to higher-cost foreign producers. This will undoubtedly prove problematic for US inflation. Notwithstanding the rapid unwinding of the Covid inflation shock, underlying inflation — which has plunged from 6.6% on the core CPI in September 2022 to just 3.3% through June 2024 — still remains well above the Federal Reserve’s 2% price stability target. My back-of-the envelope calculations suggest that the anti-China trade policies of Trump 2.0 could boost the US inflation rate by approximately 0.5% to 1.0%. Under those circumstances, recent disinflationary trends could well reverse course, prompting an inflation-targeting Fed to hold interest rates higher than might otherwise be expected.

All in all, there is little reason to expect an end to what is shaping up to be America’s forever trade war with China. While Trump started the tariff battle in 2018, Biden has broadened the anti-China campaign — sustaining Trump’s tariffs and targeting Chinese tech. The prospects of sharp further tariff increases occurring during Trump 2.0 will only intensify the US-China conflict. China’s tit-for-tat retaliatory response to the tariffs of Trump 1.0 provides a reasonable template of what to expect from the PRC in the far more extreme tariff regime of Trump 2.0. Moreover, under the guise of national security concerns, America’s penchant for increased friend-shoring and a concomitant further decoupling of China-centric supply chains will only add to the tensions of de-globalization. I worry increasingly about the mounting perils of a 1930s style global trade war.

Next week: Trump 2.0 and Taiwan

Thank you again for your in depth explanation about the deficit and how China got blamed.How revealing! Looking forward to your blog on Taiwan!