The Hypocrisy of Reciprocity

Macroeconomics is the kryptonite of Trump's Reciprocal Tariff Plan. The proposal is laced with a disdain for facts, ignorance of history, and blames others for problems of America's own making.

Sometimes the pundits have it right. The chorus of commentary is overflowing with criticism of Donald Trump’s reciprocal tariff proposal. With good reason. It is a terrible idea from virtually every perspective — economics, global stability, history, and politics.

What can possibly be said about this patently absurd idea that has not already been said? Leave it to Paul Krugman, recently unshackled from the New York Times, to make the simplest and one of the strongest arguments against Trump’s reciprocal tariff proposal. As Krugman points out in his new blog, over the past 90 years, the global trading system has, in fact, been shaped by the very reciprocity the current US president insists is missing. That’s right, following the disastrous Smoot-Hawley tariffs of 1930, the US Congress did an about-face and passed the Reciprocal Trade Agreement Act (RTAA) of 1934; signed into law by FDR, the RTAA set the stage for the establishment of the modern global trading system. Post-World War II, this took the form of the General Agreements on Tariffs and Trade (GATT) that ushered in eight rounds of reciprocal cuts in global tariffs.

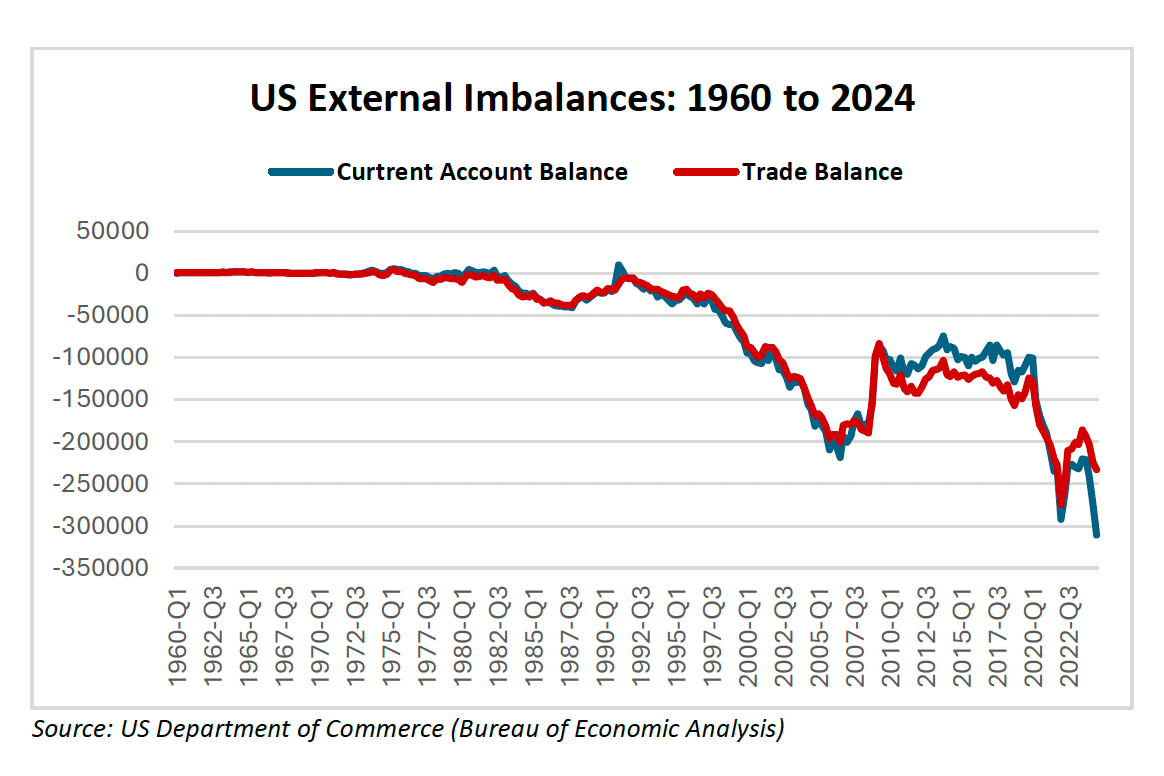

Yet today’s MAGA reciprocalists are not just ignorant of the modern history of global trade policy, but they and their leader — an economics major at Wharton — also lack a basic understanding of macroeconomics. Here, I am obviously talking my own book — several books, in fact, and countless articles. My argument, hardly an esoteric theory, rests on the basics of national income accounting — namely, that an economy’s current-account balance is the difference between domestic saving and investment. That’s where trade deficits enter the equation. In the United States, there is almost a one-for-one correspondence between the current account and the trade balance (chart below). In other words, our gaping and seemingly chronic trade deficit is less a manifestation of a lack of reciprocity by our trading partners and more a direct outgrowth of America’s homegrown macroeconomic tensions — the gap between investment and saving.

A macro perspective is important because it frames America’s trade deficit debate in multilateral terms — deficits with 101 nations in 2024, for example — rather than in bilateral terms, as the widely accepted "China shock” hypothesis would lead you to believe. That means as long as the shortfall of domestic saving persists, country-specific remedies for a gaping trade deficit won’t work. That’s right — irrespective of punitive tariffs aimed at one country, or even a group of countries, the US will still need to import surplus saving from abroad and run massive current account and multilateral trade deficits with many countries to attract foreign capital. The composition of the multilateral trade deficit might change for a number of reasons — tariffs, shifting supply-chain connectivity, or trading practices of individual partners — but the overall trade deficit is determined by the macro saving-investment imbalance.

Consider the facts: Over the 2018 to 2024 period, which spans the first phase of the Trump-Biden tariff war, the net domestic saving rate sunk to just 1.8% of national income — a fraction of its 7.6% average over the final four decades of the 20th century (1960-99) — and as of the third quarter of 2024 stood at just 0.4%; over the same period, the overall merchandise trade deficit widened from $879 billion in 2018 to a record $1.2 trillion in 2024. Predictably, as China was squeezed by tariffs, trade diversion kicked in; the Chinese piece of the multilateral deficit shrank but other, largely higher-cost, trading partners more than filled the void — namely, Mexico, Vietnam, Canada, South Korea, Taiwan, India, Ireland, and Germany. For a saving-short US economy, the outcome was like rearranging the deck chairs on the Titanic.

Macro is the kryptonite of Trump’s tariff reciprocity proposal. Not only does it explain trade diversion, but it raises an even deeper issue for a saving-short US economy. It puts the onus squarely on the largest source of America’s saving shortfall, the federal budget deficit. In the true spirit of reciprocity, the rest of the world could just as easily turn America’s protectionist case inside out, insisting that the US finally come to grips with its responsibility for solving the trade problem by committing to a credible program of federal budget deficit reduction. Washington, of course, has ducked that responsibility since the 1970s, and the likelihood of outsize budget deficits during Trump 2.0 will only exacerbate already tough macro circumstances. US politicians prefer to address the symptoms rather than the source of a problem. Donald Trump is classic in that regard.

Conveniently, the President has left it up to others to provide the rationale for reciprocity. Robert Lighthizer, US Trade Representative (USTR) in Trump 1.0, initially took the lead, reinforced by the recently incarcerated Peter Navarro, who served as trade advisor in both Trump administrations and was also the co-author of the tariff manifesto that appears in Chapter 26 of Project 2025. Of the two, Lighthizer, as a frequent op-ed contributor and recent book author, has attempted to play the more serious intellectual role in leading today’s reciprocity movement; like many, I was surprised he was not appointed the “trade czar” of Trump 2.0, as had been widely leaked after last November’s election. That left his acolyte, Navarro, much closer to the center of power.

The result, in keeping with Peter Navarro’s contribution to Project 2025, is the “Reciprocal Trade and Tariffs,” plan outlined in a presidential memorandum of February 13. Section 1 of The Plan, laced with gobsmacking, is framed around the inarguable realization that “our Nation [is] dependent on other countries to meet our security needs.” As if there is really any choice for a saving-short US economy!

Apart from the trade deficit, The Plan also contains a long list of complaints about other unfair trading practices of our economic adversaries that are alleged to have inflicted egregious harm on “American workers, manufactures, farmers, ranchers, entrepreneurs, and businesses.” Singled out are industrial policies, value-added and other extraterritorial taxes, currency manipulation, and a catch-all category of “any unfair limitation or structural impediment to market access” that impinges on the free and fair competitiveness of the US economy.

This laundry list is basically a rehash of the original Section 301 Report authored by then USTR Robert Lighthizer in March 2018 that attempted to justify the tariff war against China. The only difference is that the current allegations are lodged against all of America’s trading partners, friend and foe alike — including Canada, Mexico, Europe, and Japan, to say nothing of going after China again. Last time, the tariff campaign fixated on China.

My criticism of the original Section 301 Report, detailed in Chapter 4 of Accidental Conflict, is still appropriate today. I stressed that virtually every nation relies to some extent on industrial policy — including Japan, Germany, China, and, most recently, the United States with its Chips and Science Act, the Bipartisan Infrastructure Bill, and the green technologies of the Inflation Reduction Act of the Biden Administration, now followed by the AI Action Plan of Trump 2.0. The evidence on currency manipulation is weaker today than it was back then. The only thing new is an absurd case that the Trump reciprocity plan makes against the VAT (value-added tax), condemning other nations for opting for a different tax system that is actually a far more equitable and efficient way to raise revenues at all stages of today’s increasingly complex production process; moreover, as many have argued, a VAT-based consumption tax might be exactly what a saving-short, deficit-prone US economy needs.

Obviously, my macro arguments doesn't fit too neatly into today’s MAGA-driven political equation in the United States. As the man who famously launched his first presidential campaign with a trip down the golden escalator, it is only fitting that Donald Trump has become the apostle of a new Golden Rule of reciprocal political action: Do unto others what you insist they have done, or are doing, to you. That is not only evident in a domestic retribution campaign against the imaginary conspiracies of the Deep State but is now glaringly evident in a new confrontational campaign of international economic policy.

The MAGA wrecking ball is now taking dead aim on the global order, not just driving a wedge between America, Ukraine, and the rest of Europe, but also shredding the norms of world trade. Trump’s so-called Reciprocity Plan is laced with a disdain for analytics, a dismissal of fact, ignorance of history, and a dangerous hypocrisy that blames others for problems largely of America’s own making. It deserves a prominent place in the dustbin of incoherent policy proposals.

“…the recently incarcerated Peter Navarro…”. Who is working for a recently convicted felon who has assembled a clown car or is it a prison cell of the bottom of the barrel scum. Most of these losers including Trump himself couldn’t get hired as a greeter at WalMart

If I had a penny for the number of analysts who continue to view tariffs from simply the perspective of trade, I'd be a rich man. Tariffs are more importantly about capital flows. You complain about low savings and correctly point out that the biggest driver is government deficits. We'll see how much Trump can cut but you should consider deregulation too and it's impact of domestic savings. Secondly, it's an incomplete analysis if you're not willing to consider tariffs as a tool of negotiation and view tariffs not simply from the perspective of the US but also from that of other countries. I have argued in my posts that reciprocal tariffs will result in globally lower tariffs, not higher. Finally, nothing ever works linearly and you should consider the impact of both the rising dollar and deficit positions of other countries to realize what the equilibrium solution might be. It may never be reached but at least you'll know where the information asymmetries lie.