Squandering a US-China Summit?

What is missing from the upcoming Beijing agenda

It’s pretty obvious by now how much Donald Trump and Xi Jinping want to cut a deal at their upcoming April summit in Beijing. Trump has continued to vent his anti-globalist hostilities on friends and foes, alike — with the notable exception of China. Xi has kept a lower profile, but all signs suggest that the Chinese are moving ahead actively with summit planning — despite concerns that Xi conveyed on a recent phone call with the US president over pending US arms shipments to Taiwan.

A deal, of course, is Trump’s persona. By contrast, the Chinese view deals through a strategic lens. This reflects the very different character of both systems — America’s myopia in seeking the quick fix and China’s longer-term strategic perspective of laying out a succession of five-year plans to shape their future trajectory.

Irrespective of these different perspectives, China and the US both face comparable macroeconomic challenges that will ultimately require serious attention. The two nations are joined at the hip through structural saving imbalances. The United States suffers from a chronic shortfall of saving and a massive current account deficit while China has the largest surpluses — saving and the current account — of any nation in the world.

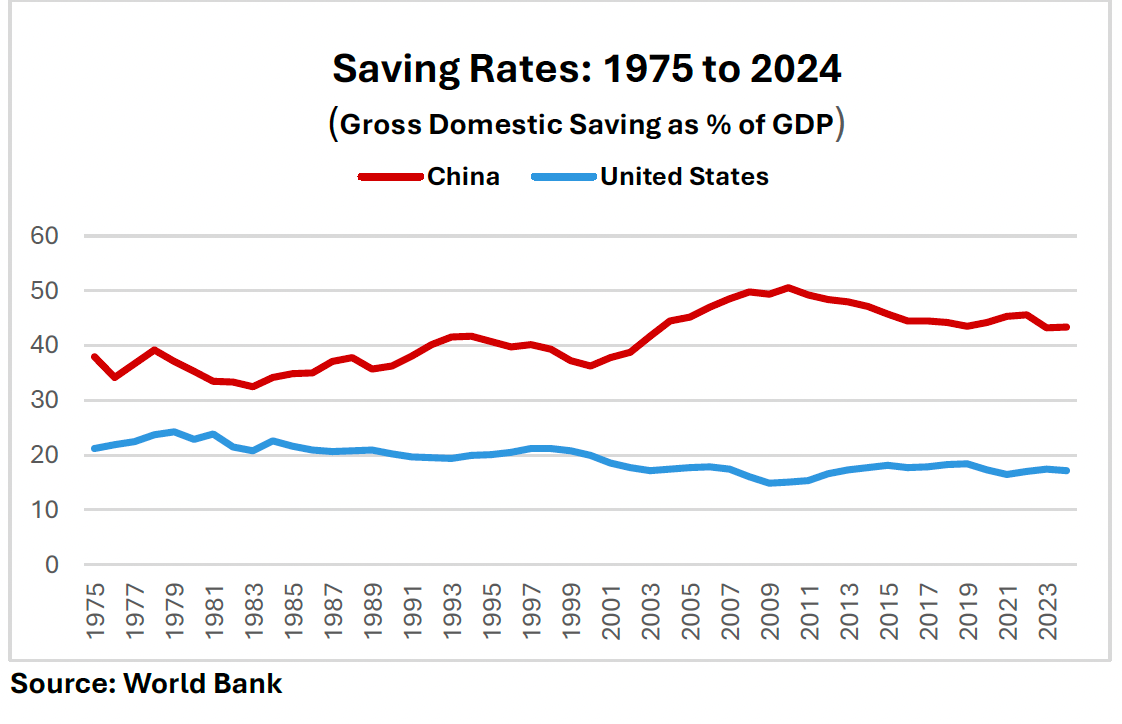

In the US, the net domestic saving rate — the sum of net saving from the household, business, and government sectors — has averaged just 2.1% since 2000 (and only 1.0% since 2020). That is far short of the average of 7.6% recorded over the prior 40 years from 1960 to 1999. China’s gross national saving rate — a slightly different construct that includes depreciation of worn-out capital — averaged 44.9% of GDP from 2000 to 2024. For major economies, that is more than seven percentage points above China’s 37.2% average over the prior twenty years, from 1980 to 1999 (see chart below).

The contrasting imbalances between the US and China are essentially mirror images of each other. Needy of surplus saving from abroad in order to invest and grow, the US borrows freely from the world’s surplus saving economies, like China. China, of course, is not the only surplus saver in the world — although it certainly has the biggest pool of excess saving; others include Japan, Germany and, to a far lesser degree, South Korea. But, seen together, these twin imbalances basically paint a picture of voracious American consumers drawing freely on the saving surpluses of repressed Chinese consumers. In other words, China’s frugality enables America’s profligacy,

The connection between structural imbalances and the economic growth imperatives of China and the United States is open to debate. So far, China’s current account surplus has not been a serious problem. However, to the extent it persists — and it increased sharply again starting in 2025 — China is likely to face a growing protectionist pushback from the rest of the world for upping the ante on its mercantilist, export-led growth strategy.

Similarly, the US has been able to sustain economic growth despite its saving and current account deficits, in large part because its ability to borrow from abroad has been supported by the “exorbitant privilege” of a strong US dollar. If the dollar ever weakens enough to challenge its dominant reserve status, the US may lose that special privilege. America’s deficit-fueled growth could then be in serious trouble.

Like China’s case for consumer-led rebalancing, there is an equally compelling case for saving-led rebalancing in the United States. Yet for both nations there have been no meaningful signs of major shifts in that direction. The inertia in China is traceable to household sector fear of an uncertain future that encourages excessive precautionary saving. The inertia in the US reflects the lack of an interest rate penalty for outsize budget deficits, as well as surging asset-based saving generated by long frothy equity markets.

That contrast points to the possibility of very different triggers for rebalancing in the two nations. For China, the spark could come from reforms and policy shifts, as well as from the aspirational value proposition of an increasingly flourishing consumer society. For the United States, increased saving is more likely to be a market-driven phenomenon reflecting the possibility of congestion in Treasury funding markets and/ or a major equity market reversal of the highly concentrated bet investors have made on major AI companies in recent years. Which comes first — a shift in Chinese policy or a sharp correction in US asset prices?

That’s a tough call. But there may be a silver lining. While we tend to stress the mounting risks of unsustainable imbalances, we shouldn’t lose sight of the opportunities they offer. China needs more consumer-led growth. Who better to learn from than the American consumer, the most powerful consumer in the world? That’s especially the case for consumer services such as transportation, tourism, cultural institutions, and “lifestyle” services that are the focus of a new “work plan” just unveiled by the Chinese leadership. Similarly, the US focus on a revival of manufacturing could benefit from lessons learned in China’s recent advances in logistics, distribution, and robotics.

Moreover, both nations face long-term productivity challenges. There is general agreement that innovation and technological advances play especially important roles in boosting longer-term productivity. That brings artificial intelligence to the fore for China and the United States as a key pillar for prospective trends in productivity and longer-term economic growth. Both countries, currently locked in a zero-sum competition over AI supremacy, could benefit enormously by adopting a more collaborative approach to reaping the benefits from this revolutionary development.

Notwithstanding these mutual opportunities, as long as both nations remain mired in conflict, they may be reluctant to engage in a spontaneous sharing of best practices. The US and China are organized as two very different, highly competitive, systems — free-market capitalism and market-based socialism. Conflict resolution can’t happen without mutual acceptance of those differences.

In looking to the upcoming Beijing summit, it is important to stress that another bilateral trade deal will not address these macroeconomic imbalances. That was the case with the failed “Phase I” trade deal of 2020, and yet there are hints that both sides are going to try the same unworkable approach again at the April summit. I am a broken record on the point that there is no bilateral trade fix for a multilateral saving/ trade problem. If all the April summit delivers is another misplaced trade deal, it will have squandered a major opportunity.

None of this seems to manner to a deal-fixated Donald Trump. His counter to conflict with China: don’t worry, he and Xi are “good friends.” Irrespective of whether that is correct, superficial claims of camaraderie are unlikely to carry much weight in resolving a seriously conflicted Sino-American relationship. Xi remains less interested in friendship and more focused on strategy. Remember Sun Tzu: “When your strategy is deep and far reaching … you can win before you even fight.”

The meaningful evidence of major shifts are appearing in markets