Delusions, Markets, and Bubbles:

The likely bursting of an AI bubble could be a far more serious problem than the Dotcom bust of a quarter century ago.

As an economist, I have long been mindful of my limits in making market calls. I have had my share of hits and misses — correctly warning of equity bubbles in 1987 and 1999 while mistakenly sounding the alarm on a crash in the US dollar in 2021. Barton Biggs, my erstwhile mentor at Morgan Stanley, had little patience for the market views of economists. I felt the same about the economics insights of market strategists. But Barton and I were great friends, and I have always treasured an old, cracked crystal ball that he left me. In that spirit, bear with me as a tough message comes into focus.

This tale is, first and foremost, about delusions — not exactly in short supply these days. There is a seemingly endless torrent of political delusions evident in the early days of Trump 2.0. Think Gaza — or Greenland, the Panama Canal, or even Canada. My focus, however, is on the delusional proclivity of financial markets, a tendency with deep historical roots that are well documented in Charles Mackay’s 1841 classic, Extraordinary Popular Delusions and the Madness of Crowds. Originally a three-volume opus, Mackay’s case had three legs to the stool — national delusions (mainly economic bubbles), peculiar follies (such as crusades and witchcraft), and philosophical delusions (mainly alchemy). While written nearly two hundred years ago, the book has great cultural relevance in capturing the speculative fervor behind many of the subsequent delusionary episodes that were to come in financial markets.

That is especially the case with recent asset bubbles. The dotcom and subprime bubbles of the late 1990s and early 2000s are especially noteworthy — both delusional episodes of asset speculation that sparked major collateral damage in financial markets and the real economy. To Yale Professor Robert Shiller, asset bubbles occur when speculators buy in anticipation of future price increases; the corollary of his research finds that bubbles usually burst under their own delusionary weight — in other words, it doesn’t take much of a pin prick to shatter the delusion and puncture the stretched membrane of an asset bubble.

Context is especially important here. Thanks to a legacy of low inflation and über-accommodative monetary policy, financial markets have enjoyed extraordinary support from a protracted period of exceptionally low interest rates. However, due to the lingering inflationary impacts of post-Covid supply shocks, those days appear to be over. That has led to an important transition from rock-bottom to more normal interest rates; the benchmark 10-year yield on US Treasuries went from less than 1% in 2020 to 5% in October 2023 and currently stands at little under 4.5%. Since 1962, nominal yields on 10-year Treasuries have averaged 5.85%; consequently, while there may be more to come in the interest rate normalization process, it seems safe to say that, barring another unexpected spike in inflation, the bulk of the move is now in the past.

The near normalization of long-term interest rates is important in that it allows us to disentangle valuations in other asset markets from comparisons with once seriously over-priced Treasuries. As such, it provides a cleaner read on valuation excesses elsewhere in the financial system. With that in mind, I go back to the crystal ball and draw your attention to two worrisome bubbles — the possibility of an AI bubble that I will now turn to and, yes, another warning of a dollar bubble that I will address next week.

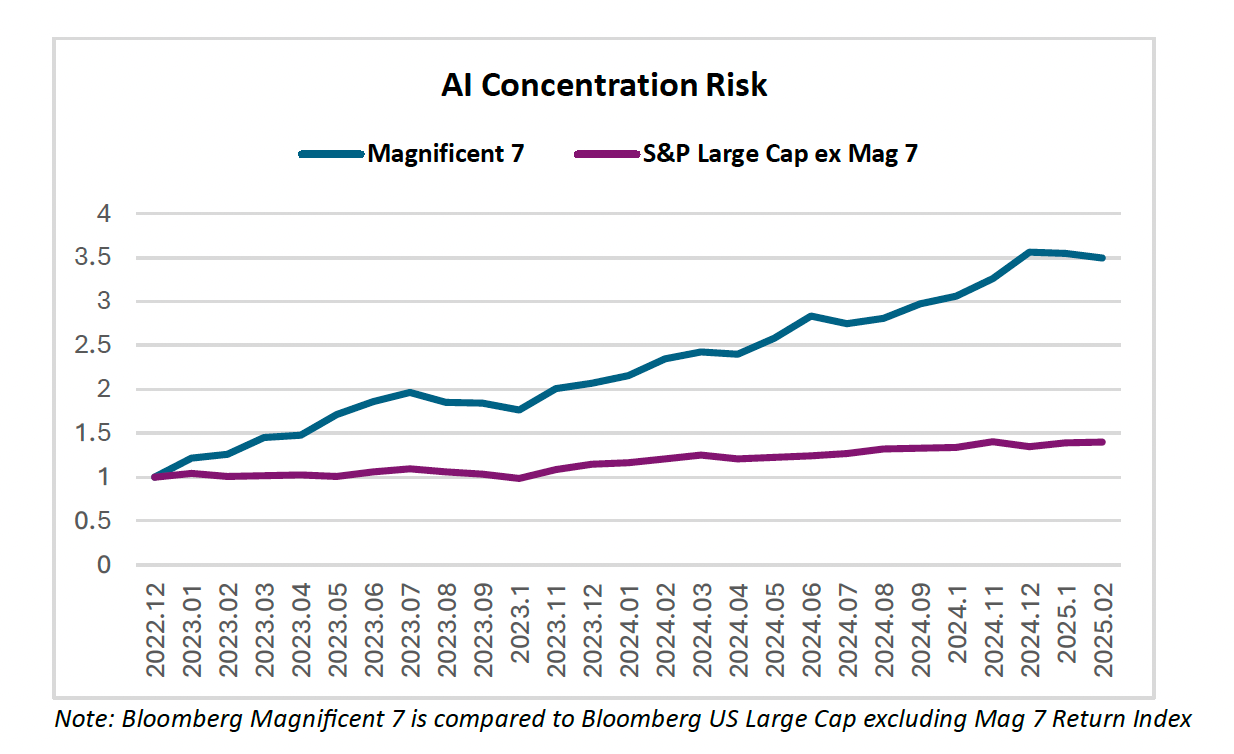

There can be no mistaking the froth in AI-related assets. As shown in the chart below, the so-called “Magnificent 7” — an AI-sensitive grouping of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla — is up fully 3.5 times (as measured on an equal-weighted total-return basis) from year-end 2022. This surge goes well beyond the admittedly impressive earnings of these companies; the Mag 7 price-earnings ratio of 41.5 is more than 60% higher than the 25.3 multiple for other large capitalization stocks. Notwithstanding the one-day selling spasm of January 27 due to the DeepSeek scare, there seems to be no stopping the AI mania.

The chart above also underscores the contrast between the current AI-related surge and the Nasdaq bubble of late 1999 and early 2000. We all know the saga of that earlier demise; as per Shiller’s diagnosis, the dotcom bubble collapsed under its own weight in an unfriendly Fed environment (sound familiar?). Predictably, intra-asset contagion led to a carnage that spread well beyond the dotcom sector; from its March 2000 intra-day peak, the Nasdaq composite index collapsed by 78% over the following 21 months while the broader S&P 500 index plunged by 48% in the three years following the Nasdaq peak.

Significantly, there is far greater concentration risk in the equity market today than there was back then (chart below). By December 2024, the Mag 7 accounted for fully 34% of the total market capitalization of the S&P 500 — nearly six times the 6% market cap share of internet companies in March 2000. On that basis, today’s equity market is far more dependent on a technology bet than it was a quarter of a century ago. In other words, the stakes of delusion risk couldn't be higher.

It's not just the AI valuation comparisons that trouble me. My concerns over an AI bubble are also rooted in the Japanese experience of the late 1980s and early 1990s. Japan’s bubble economy was distorted by the interplay between excesses in asset markets and the real economy — specifically, in the form of a surge in business capital spending that Corporate Japan justified on the basis of bubble-related valuations in Japanese equities. Japanese companies were deluded into believing that they literally had to expand in order to justify their lofty valuations.

Today’s AI behemoths are afflicted with an analogous Japanese-like delusion, engaging in a capital spending binge that they believe is essential to support a massive expansion in machine-learning and data storage capacity. The combined capex for Microsoft, Meta, Alphabet, and Amazon is estimated to have hit $218 billion in 2024 — up over 45 % from average spending levels in 2022-23. Moreover, Google just announced a $75 billion capital spending program for 2025‚ up another 40% from last year. Add to that the Stargate joint venture between Open AI, Oracle, and SoftBank, with its potential capital raise of $500 billion, along with a recent announcement of a Japanese AI joint venture between OpenAI and Softbank. Just like Japan.

Delusion? You tell me. The explosive upsurge in spending by leading AI companies flies in the face of the low-cost DeepSeek alternative. The extraordinary cost efficiencies of the Chinese version of OpenAI fundamentally challenge the capex- and energy-intensive spending trajectories that underpin the current AI binge. My indictment of the AI frenzy has nothing to do with the obvious brilliance of a revolutionary innovation. However, like the dotcom bubble of the late 1990s, the market is way out over its skis. In Charles Mackay’s lexicon, the “madness of crowds” seems to be an apt description of AI valuations as yet another delusional mania. The markets may have initially shrugged off the one-day swoon associated with the DeepSeek shock. Is that the pin than pricks this bubble? Over time, I suspect there will be some serious rethinking of that critical question.

The political angle is equally important in shaping delusional excesses in financial markets. Back in the late 1990s, it was the cheerleading of Fed Chairman Alan Greenspan that played an important role in fueling the froth in dotcom. Greenspan, of course, was not a politician. But his strong conviction in what became known as a “new paradigm” was the functional equivalent of injecting political support into speculative market excesses. In effect, he gave speculators permission to indulge in a delusional market bet.

The Maestro’s intervention was not all that dissimilar from today’s political culture that celebrates the power of tech oligarchs. The MAGA cheerleading of Donald Trump, JD Vance, Elon Musk, and the rest of the broligarchy loudly proclaiming America’s supremacy in AI and crypto, amplifies the politics of delusion. The combination of delusional political leadership and financial market excesses points to an AI bubble that can only end one way. The question is when, not if.

Next week: The Delusional Dollar

Thanks for the feedback. Michael, as usual, you make very provocative points. In my haste to hit the send button last night, I pushed out an early version that overlooked a critical point. The third paragraph from the end should read as follows:

“Delusion? You tell me. The explosive upsurge in spending by leading AI companies flies in the face of the low-cost DeepSeek alternative. The extraordinary cost efficiencies of the Chinese version of OpenAI fundamentally challenge the capex- and energy-intensive spending trajectories that underpin the current AI binge. My indictment of the AI frenzy has nothing to do with the obvious brilliance of a revolutionary innovation. However, like the dotcom bubble of the late 1990s, the market is way out over its skis. In Charles Mackay’s lexicon, the “madness of crowds” seems to be an apt description of AI valuations as yet another delusional mania. The markets may have initially shrugged off the one-day swoon associated with the DeepSeek shock. Is that the pin than pricks this bubble? Over time, I suspect there will be some serious rethinking of that critical question.”

Always appreciate your thoughts Mr. Roach.

Whenever the opportunity presented itself, I’d dig in and read with care. I’m very happy to see you publishing here now.

Nice to see the nod for Barton Biggs too. A sage voice amongst many who were considerably less so. Wise, and humbled by time, like yourself.

Thank you.