China's Trump Cards

China's tit-for-tat response to the latest US export sanctions hints at a retaliatory race to the bottom in a Trump 2.0 tariff scenario.

In a long overdue move, the US has just updated its restrictions on high-bandwidth memory chips and the foreign direct product rule for semiconductor manufacturing equipment, while also adding another 140 Chinese companies to the Commerce Department’s entity list. As has been the case since 2018, China has been quick to counter-punch, in this case with a tit-for-tat response banning US purchases of several critical minerals — gallium, germanium, antimony, and “superhard” materials — while tightening controls on graphite. This hints at what could well lie ahead if Donald Trump delivers on his campaign promise to up the ante on Chinese tariffs. Retaliation is the high-octane fuel of conflict escalation.

I have written two books and countless articles on the mounting perils of US-China codependency. This is at odds with a Washington consensus that harbors the notion of a one-way dependency, that that China is beholden to the United States as the largest consumer market and leader in new technologies. I have argued, instead, that the United States is also heavily dependent on low-cost Chinese goods to make ends meet for income-constrained consumers; that the United States depends on Chinese surplus saving, especially its purchases of Treasury securities, to help fill its void of domestic saving; and that US producers depend on China as America’s third largest and most rapidly growing export market. Codependency, in short, means that we depend on China just as much China depends on us.

Donald Trump refused to accept this logic in his first term and seems unlikely to change his tune in his second term. Accordingly, it makes sense to revisit the consequences of Trump 1.0 in order to think about what might happen in Trump 2.0. Back then, in a series of actions, US tariffs on Chinese products were raised from 3% in 2016 to an effective tariff rate of 19% by 2020 and have held at that level throughout the Biden Administration. Trump, ignoring the macro ramifications of a saving-short, deficit-prone US economy, held the mistaken view that there was a bilateral (China) fix for a multilateral trade deficit (with 106 countries).

That backfired. Over the subsequent years, the overall US merchandise trade balance widened from -$879 billion in 2018 to -$1060 billion in 2023. Predictably, in response to tariffs, the Chinese share of the overall US trade deficit fell from 47% to 26% over this same five-year period. However, the Chinese potion of the US trade deficit was simply diverted to Mexico, Vietnam, Canada, Korea, Taiwan, India, Ireland, and Germany. I have estimated that more than 70% of the $319 billion in trade diversion away from China went to higher-cost or comparable-cost nations, underscoring the key conclusion that trade diversion is the functional equivalent of a tax hike on US companies and consumers.

Expect more of the same in a second Trump Administration. No one, including the president-elect, himself, knows for certain what Trump 2.0 ultimately implies for tariffs. But it seems reasonable to expect that Donald Trump will stick with his campaign promise to raise tariffs on China by considerably more than hikes to be imposed on other trading partners. During the recent election campaign, Trump threw out numbers of 20% and 60% for global and Chinese tariffs, respectively. I suspect he will ultimately settle for something less. But whatever the final tariff rate, it is important to stress the flawed logic of this approach — that imposing a steeper penalty on the largest bilateral piece of a multilateral trade deficit with many countries won’t work. As long as domestic saving remains suppressed by outsize federal budget deficits, as the likely fiscal policy of Trump 2.0 suggests, a China-centric “remedy” will simply lead to another round of trade diversion that will further penalize US producers and consumers.

China’s just-announced retaliatory actions on critical minerals underscore another visible manifestation of a codependent trade conflict — a surgical strike that has the potential to crimp US production of a wide range of strategically important goods, from semiconductors and satellites, to infrared technology and fiber optic cables, to lithium batteries and solar cells. That’s especially the case for germanium where China accounts for fully 50% of US imports of that critical mineral (see figure below). The message is unmistakable: China has the capacity to inflict strategic damage on the US that is quite comparable to what Washington is seeking through its “small yard, high fence” China containment strategy. As I have stressed repeatedly, codependency cuts both ways — especially now as the Biden Administration in its waning days is attempting to make the metaphorical yard smaller and the fence even higher.

Ultimately, the codependency framework behooves us to think about broader retaliatory efforts by China and America’s other trading partners. So far, China’s responses have been relatively narrow, matching US product-specific sanctions with comparable strategic restraints of its own. In effect, the latest tit-for-tat of China’s critical minerals has been paired with a tightening of US export controls aimed at Chinese domestic semiconductor development and artificial intelligence.

But the narrow aperture of the codependency lens has the potential to go considerably wider. That could be especially the case in a Trump 2.0 scenario that includes sharp across-the-board increases on Chinese tariffs as well as sanctions along the lines suggested in Project 2025, especially Chapters 21 (on the Commerce Department and decoupling) and Chapter 26 (on the tariff manifesto of trade policy). To the extent that Donald Trump follows even part of the script that he disingenuously disavowed during the campaign — “I have nothing to do with Project 2025” — the Chinese can be expected to respond far more forcefully that their latest targeted actions might suggest.

What a broader Chinese response might look like is, of course, very hard to tell. But, here as well, the codependency framework offers some important hints. By its latest actions on critical minerals, China has opened up the possibility of turning its trade with the United States into an even broader strategic weapon; that would include the potential for wide-ranging constraints on rare earths, which are of enormous strategic importance to the United States in many critical product lines, from military defense and battery production to smartphones and specialized magnets used in motors.

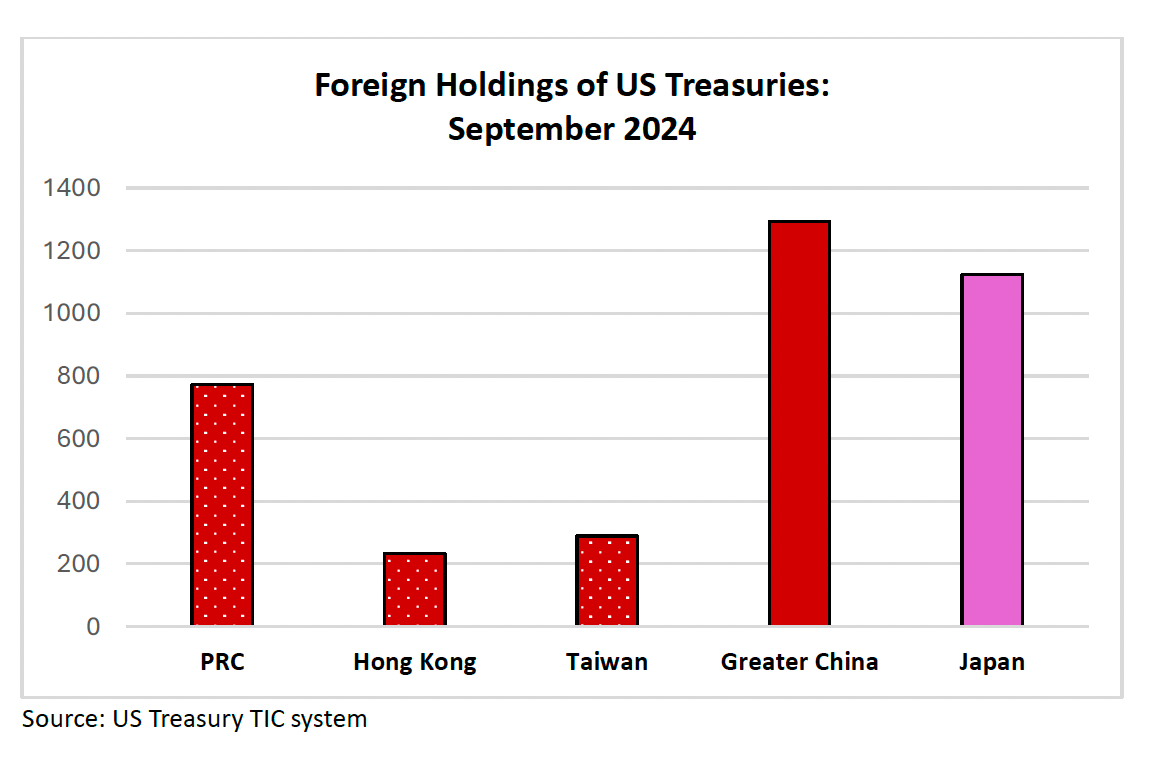

Then, of course, there is the ultimate financial weapon — Greater China’s $1.293 trillion in direct holdings of US Treasury securities ( including $772 billion by the PRC, $233 billion by Hong Kong, and $288 billion by Taiwan, all as of September 2024). Whenever I even hint at this option, it is quickly dismissed by cavalier Americans who typically respond, “They wouldn't dare — it would hurt them more than us.” There are several ways to think of this, as I outlined in a “bad dream” sequence of my 2009 book, Unbalanced: China could go on a buyer’s strike during upcoming Treasury auctions, or, even more extreme, it could start to unload its outsize position as America’s largest foreign creditor (as measured on a consolidated Greater China basis) ahead of Japan. Either option would be devastating for America’s deficit-prone economy and would unleash havoc in the US bond market, with wrenching collateral damage in world financial markets. While it sounds almost suicidal for China to spark such a financial meltdown, it is equally reckless to dismiss the consequences of a trapped adversary. As such, it is important to be mindful of the extreme “tail risks” of a conflicted codependency.

Much of the post-election policy discussion has focused on the tariff initiatives likely to be forthcoming in Trump 2.0. Sino-American codependency urges us to think less about unilateral actions and more about the retaliatory responses to those actions. Donald Trump’s nationalistic view of “America First” ignores how much a saving-short US economy depends on China and the rest of the world for goods and financial capital. Under Trump 2.0, America’s budget deficit and domestic saving shortfall could well go from bad to worse. In a codependent Sino-American relationship, that means China is hardly lacking in “Trump cards.”

I might be wrong, but I think China simply prohibits the military use of those resources, but not their civilian use.