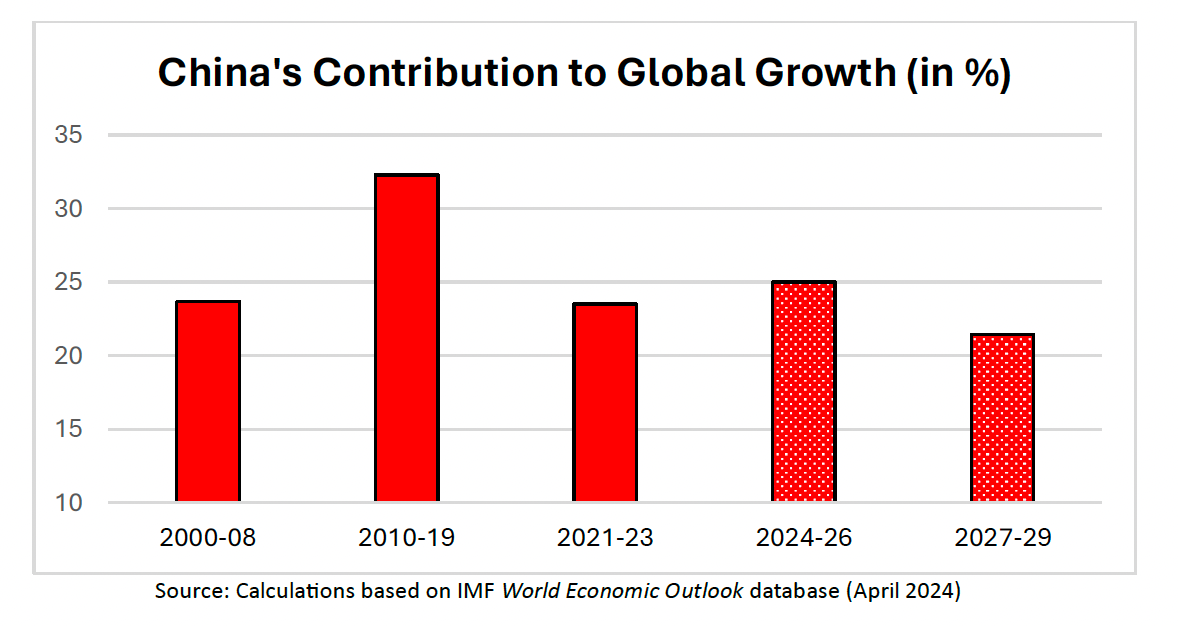

A proud Chinese leadership has long boasted of the important role that China has played as the major engine of global growth. The numbers certainly bear that out. Over the ten-year period, from 2010 to 2019, China accounted for fully 32% of the cumulative increase in world GDP. No other country, or economic grouping, came close to matching the global impetus provided by the great Chinese growth engine.

Many in the West have endorsed this narrative. I confess to having been one of the more ardent cheerleaders of China’s increasingly powerful role in supporting the global economy. In a 2016 article, “The World Economy Without China,” I argued that vigorous Chinese economic growth was the only thing that stood between a fragile recovery and a recessionary relapse in in the global economy in the years immediately following the Global Financial Crisis of 2008-09. When I wrote that article nearly eight years ago, I warned that there could be serious consequences for the rest of the world if the Chinese growth engine were to slow.

Those fears are now coming into focus. Over the past three years, 2021 to 2023, China accounted for just 23% of total global growth, nine percentage points less than the record 32% contribution in the decade ending in 2019. Moreover, in looking to the future — taking the IMF’s latest (April 2024) World Economic Outlook as an approximation of a baseline prognosis — the Chinese global growth contribution appears likely to fade further. As the figure below indicates, Chinese GDP growth is projected to account for just 21% of the cumulative increase in world GDP over the three-year period from 2027 to 2029.

Don’t get me wrong. Even with such a diminished growth impetus, China is still a big deal for a world where economic growth is in short supply. But its 21% contribution to global growth projected for 2027-29 would be smaller than at any point since 2000. It would bear a closer resemblance to the role that China played in the earlier days of its growth revival, when over the two decades of the 1980s and the 1990s, it accounted for about 15% of the cumulative increase in world GDP. Based on the IMF’s latest forecast, China appears to be on a trajectory that is reverting to its earlier role — delivering roughly in accordance with its weight in the mix of world GDP.

And that gets to an important consideration that underpins these calculations. The Chinese growth contributions as described above are measured on a purchasing power parity (PPP) basis — adjusting for disparities in living standards that can distort cross-country comparisons. PPP is a widely accepted metric that has long been used by the IMF and others to effectively add up the pieces of the global economy. It is far preferable to alternatives measured in US dollars, which are subject to the whims of ever-volatile foreign exchange markets that can seemingly boost or depress a country’s GDP solely on the basis of fluctuating currency values, rather than reflecting more meaningful shifts in real economic activity.

As can be seen in the table below, China’s PPP-based contributions to global growth basically reflect two pieces of information — the real growth in its economy and the share of its economy in a PPP-based world. What’s particularly interesting about the coming reduction of China’s global growth impetus is that it reflects not just a projected slowdown in real GDP growth but also a flattening out of its share in world GDP.

As the table indicates, during the first two decades of the 21st century, the power of the Chinese growth engine — China’s share of world GDP growth — reflected the combination of strong Chinese GDP combined with China’s sharply rising share of world GDP; by 2019, the PPP share of 17.2% was over six times the 2.7% share in 1980 when China’s modern growth story began. That was critical in allowing China’s growth engine to deliver at peak performance in accounting for a record 32% of the gain in world GDP in 2010-19 as noted above.

Significantly, this was not due to surging economic growth, which, in fact was already in the early stages of a slowdown — going from the post-1980 pace of around 10% to an average of 7.7% over 2010-19. At work, instead, were further large increases in China’s PPP share of world GDP. Had China’s PPP share remained constant over that ten-year period at the 2010 level of 13.6% rather than rising to 17.2% by 2019 as was actually the case, China’s share of world GDP growth over that period would have been 28% rather than 32%. Putting it another way, the scale effects of China’s sharply rising share of the world economy accounted for about half the increase in its global growth contribution during the 2010-19 period.

This movie is now starting to run in reverse. At work over the past three years (2021-23) are the twin forces of slower Chinese GDP growth to 5.6% (from 7.7% in 2010-19) and a much smaller increase in China’s PPP share. The IMF’s forecast for 2027-29 is particularly revealing: a slowing of average real GDP growth to just 3.4% — by far, the weakest growth performance of the post-1980 era — is expected to be reinforced by the smallest increase in China’s PPP share in modern (post-1980 ) experience. The counter-factual of further steady increases in China’s PPP share of world GDP would have boosted its projected global growth contribution in 2027-29 from the 21% share shown in the table above to around 24%, much closer to the projected average of the proceeding several years.

China has played a major role in the ebb and flow of the global economy over the past several decades. That is still the case today, even though its impetus to world economic growth is now on the wane. As China’s high-performance growth engine now starts to sputter, there will undoubtedly be important implications for other economies that have become heavily dependent on more support from Chinese growth, including commodity exporters, China’s Asian trading partners, and major advanced economies with strong linkages to China (like the US, Germany, and Japan). Moreover, absent the support of stronger Chinese growth, a more slowly growing world economy will find itself lacking the resilience it may need to withstand the inevitable next shock. All this raises an important question: Who, if anyone, might fill the void?

Next week: An answer.

Isn't rising share of PPP simply a consequence of faster growth relative to global?