Denial is among the most powerful of all human defense mechanisms, and particularly troublesome for policymakers and governments. Denial came through loud and clear during my recent post-election tour to four cities in Asia — Hong Kong, Shenzhen, Beijing, and Singapore. Not only is China unwilling to admit the severity of its economic problems, but other officials across Asia seem inclined to believe in the likelihood of an early 2025 summit between Donald Trump and Xi Jinping that will set the stage for another trade deal.

I saw nothing but denial in my recent post-US-election tour of Asia, with stops in Hong Kong, Shenzhen, Beijing, and Singapore. Taking a cue from surging global equity markets, Asians are making every effort to wish away problems at home and abroad.

Nowhere is this more evident than in China. President Xi Jinping has long stressed his preference for the “good stories of China.” Amid the most serious Chinese economic slowdown since the 1970s, government attempts to put a positive spin on the country’s outlook have intensified. An improvement in equity-market sentiment – by October 8, the CSI 300 was 35% above its low on September 13 – was the first talking point in all my discussions. Never mind that this rebound, which has since partly reversed, is purely the product of state intervention.

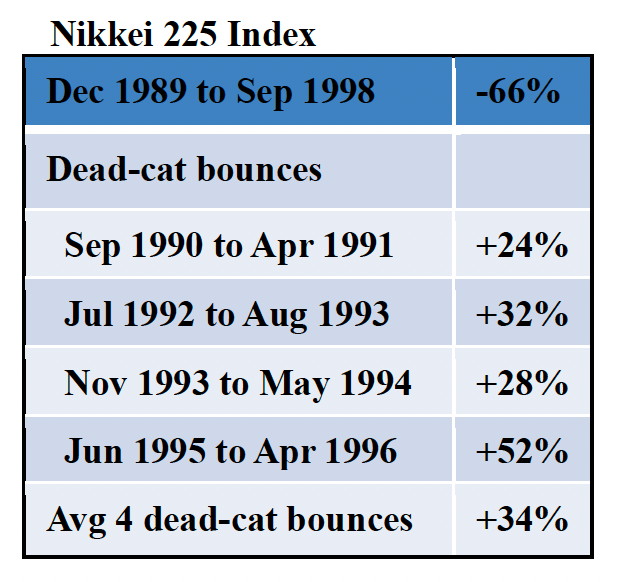

Equity markets, of course, are notorious for sending false signals. That is certainly true of bear markets, which Nobel laureate economist Paul Samuelson famously quipped predicted “nine of the last five US recessions.” It was also the case with Japan’s infamous dead-cat bounces: the Nikkei 225 rallied four times by an average of 34% on its way to a cumulative decline of 66% between December 1989 and September 1998. Nevertheless, the Chinese are clinging to recent stock-market gains as proof that their latest stimulus plan will prompt a robust economic recovery.

The Japan comparison hits a raw nerve in China. I had a particularly frustrating discussion with a senior Chinese regulator who admitted to being concerned about sharp declines in property and equity markets, the country’s mounting debt, the first whiffs of deflation, and headwinds arising from weak productivity and an aging workforce. When I pointed out that these were classic characteristics of Japan’s balance-sheet recession, the same official was quick to reject that possibility.

I did not mention the warning, issued in May 2016 by an “authoritative Chinese person” on the front page of People’s Daily, the official state organ, that China could fall into a Japanese-like quagmire. Nor did I bring up Premier Wen Jiabao’s prescient 2007 description of the Chinese economy as “unstable, unbalanced, uncoordinated, and unsustainable.” Despite making these points repeatedly in China over the years, I chose to bite my tongue on this occasion. Perhaps I was still smarting over having been silenced at the China Development Forum earlier this year by organizers only interested in the good stories of China.

But there is far more to this latest wave of Asian denial than China’s unwillingness to admit the severity of its problems. I was particularly struck by the inclination to ignore the adverse consequences of a potential trade shock should President-elect Donald Trump deliver on his campaign promise to raise US tariffs by as much as 20% on all imports and 60% on imports from China, a promise he has since reiterated.

The consensus view in Asia is that Trump is bluffing to secure an early deal. After all, he took a similar approach to his first tariff war with China in 2018-19, culminating with the ill-fated “phase one” trade deal of 2020. Given its weakened economy, many believe that the Chinese government will be even more compliant today than it was back then. Asia is abuzz with talk of an early 2025 summit between Trump and Xi that could set the stage for another US-China deal.

This recalls what played out in 2017. Back then, Trump and Xi met for two glitzy summits, featuring lavish dinners at Mar-a-Lago and in Beijing. Trump, especially enraptured with the historic surroundings of the Forbidden City, turned to Xi with bromance in his eyes and said, “My feeling toward you is an incredibly warm one.” Many expect them to seize once again on another high-profile moment to cut a quick deal – or at least begin the process that might lead to one.

Memories are evidently short in Asia. When Trump and Xi were exchanging toasts in Beijing, then-US Trade Representative Robert Lighthizer was hard at work preparing a Section 301 report on unfair Chinese trading practices that would become the template for Trump’s tariff agenda in 2018-19. Despite all the fanfare, the 2017 summits were quickly followed by a trade war that is still raging today – not exactly the outcome that deal-fixated optimists in Asia seem to be imagining.

Denial was also much on display in Hong Kong. It had been nine months since I wrote my controversial article in the Financial Times, titled “It pains me to say Hong Kong is over.” With the rebound in the Heng Seng mirroring that of the CSI 300, I was repeatedly asked if I had changed my mind. When I expressed my continued concerns about the three key issues cited in my February article – the tight links between Hong Kong and the weak Chinese economy, the crossfire of the Sino-American conflict, and a darkening political climate in the aftermath of the 2019 demonstrations – my polite hosts rolled their eyes. One went so far as to give me a red baseball cap emblazoned with “Make Hong Kong Great Again.”

I have long embraced a quasi-psychological framework in my diagnosis of the US-China rivalry as bearing the classic hallmarks of codependency. My psychologist friends also remind me of something else that was evident during my most recent visit to Asia: denial is the most powerful of all human defenses.

Arguably the greater denial lies in the failure of the developed countries to adequately fund climate mitigation and adaptation. At least China has a credible plan to deal with climate change.

1) Xi is never going to be susceptible to Trump flatulent flattery. “Very warm feelings”? Diplomacy at its finest.

2) let’s compare todays US balance sheet to China and Japan shall we. Exactly zero chance the US deficit and national debt are reduced. Trump can’t see past his next tweet.

3) Does anyone relieve believe Trump/Maga can manage the economy better than Xi? I don’t.